Maximal Extractable Value (MEV) represents the potential gain blockchain validators can obtain by strategically ordering pending transactions within a block. Validators have the power to include, exclude, or reorder pending transactions, and they can use this control for financial gain.

But what is MEV exactly, and can anyone use it to their advantage?

The good news is that there are specialized MEV bots that are designed to automatically explore opportunities and maximize profits from blockchain transactions. However, using these bots still implies technical knowledge, so it’s important that you first understand how MEV works.

Another reason why it’s good to know about MEV is its potential negative impact, as manipulating transactions within a block can lead to higher gas fees paid by end users and unfair market conditions in decentralized finance (DeFi).

Today, MEV plays an important role in major blockchains, with Ethereum being the primary market due to its dominance in DeFi and Web3. MEV was initially known as Miner Extractable Value and referred to miners’ ability to arrange transactions. However, since Ethereum’s transition from proof-of-work (PoW) to proof-of-stake (PoS), the term changed to Maximal Extractable Value (MEV) to reflect the role of validators in PoS chains.

How MEV Works

MEV is possible thanks to the decentralized nature of blockchain and the control that validators can exert on transaction ordering.

All transactions in a blockchain initially land in its so-called mempool, a public space from where validators or miners pick and order them in every new block they create. You can think of a mempool as a waiting room for transactions, where validators serve as gatekeepers who decide who goes first.

In theory, validators should just shout out the names of transactions with the highest gas fees first, which they usually do. However, given that the mempool is public and visible to anyone, independent network participants, known as ‘searchers,’ use complex bots to detect arbitrage and other MEV opportunities.

These searchers aim to include certain transactions first in the next block or certain blocks. For them, the transaction order is essential for arbitrage opportunities in DeFi, as it can affect the price of tokens, create slippage, or generate liquidations. We’ll analyze a few MEV strategies below, but for now, it’s important to understand that searchers have a financial benefit in that certain blockchain transactions are prioritized or ignored by validators.

When searchers find these MEV opportunities, they pay high gas fees to validators to prioritize their transactions. The gas fees act as incentives and contribute to the MEV revenue earned by validators. Occasionally, searchers can even partner with validators directly for MEV extraction.

As you can see, while validators have full control over which transactions can be picked first in the subsequent block, they don’t receive the maximal extractable value for them. Instead, searchers gain the main benefit by implementing advanced algorithms and sharing their profits with validators.

MEV shares similarities with insider trading by exploiting privileged access, but on the blockchain, this is not illegal.

What Is Arbitrage?

Professional traders use MEV extraction mainly for arbitrage opportunities, but what is MEV in crypto arbitrage?

Arbitrage is a way to make profits by leveraging the price gap between different markets. For example, suppose Bitcoin is $100,000 on exchange A and $100,500 on exchange B. You can buy it cheaper and quickly sell it on exchange B, making an instant $500 profit.

In DeFi, traders analyze price differences between decentralized exchanges (DEXs) like Uniswap. Obviously, these differences are not as dramatic as in our example, but profits are made from high-volume trades. We’ll shortly analyze MEV arbitrage in DeFi along with other strategies.

MEV vs. Regular Transactions

Though they are technically the same, MEV transactions differ from regular ones in terms of market impact and financial benefit for certain players.

Regular transactions follow a standard process based on gas fees. In contrast, MEV exploits how transactions are ordered, allowing validators and searchers to extract additional profits.

Here is how MEV differs from regular transactions:

| Regular Transactions | MEV | |

| What are they? | Normal transactions processed on a blockchain | Transactions strategically ordered to extract additional profits. |

| How it works? | Users submit transactions, and then validators process them in order of gas fees. | Searchers scan the mempool for MEV opportunities and then pay high gas fees to influence validators to pick their transactions first. |

| Who benefits? | Users and validators. | Searchers and validators. |

| Profit mechanism | Validators earn block rewards and tips from the gas fees paid by users. | Can be manipulated by validators to maximize profits. |

| Examples | Swapping tokens, sending ETH to a friend, moving tokens between wallets. | Arbitrage, front-running, sandwich attacks. |

| Impact on Users | Transactions are predictable and executed based on fees. | Can increase transaction costs and cause poor execution for regular users. |

| Transaction order | Determined by gas price and time of submission. | Can be manipulated by validators to maximize profits. |

As you can see, regular users can be negatively impacted by doing business on a less transparent and unfair blockchain, which contradicts the principles of decentralization. Basically, users end up paying an invisible tax because of MEV.

Still, MEV extraction exists because of decentralization, and markets must learn to control it and adapt to the new conditions.

Common MEV Strategies

Here are the main examples of strategies used to extract MEV:

Arbitrage

As mentioned, arbitrage is about identifying significant price differences for the same token across different DEXs. Searchers can capitalize on the price gaps through high-frequency trading. For example, if a token’s price on Uniswap is noticeably lower than on Balancer or SushiSwap, searchers using specialized bots would buy the token on Uniswap and sell it on the other DEXs, yielding a profit.

Searchers can also take advantage of any price gaps between different liquidity pools on the same DEX. For example, Uniswap hosts tens of thousands of pools, and many of them comprise the same token, such as ETH.

Note that price differences can be available only for a few seconds or even milliseconds, which is enough for automated bots to spot and take advantage of them.

Front-running

In this strategy, specialized bots scan the mempool for large trades or potentially profitable transactions, paying higher fees to validators to prioritize their similar transactions to reach the next block first.

For example, a searcher notices a large buy order for a meme coin on Uniswap. It would then try to buy the same token ahead of the initial order and quickly resell at a higher price once the order boosts token demand on the DEX as a result of slippage.

Front-running is regarded as unethical, and in traditional finance, it is banned altogether. However, restricting it on blockchain is not possible for now, and using this tactic for MEV extraction is a popular way to generate profits.

Front-running is especially popular with new tokens with low liquidity, where a single large trade can cause slippage. In fact, this strategy is so common that some bots are trying to front-run other front-running bots.

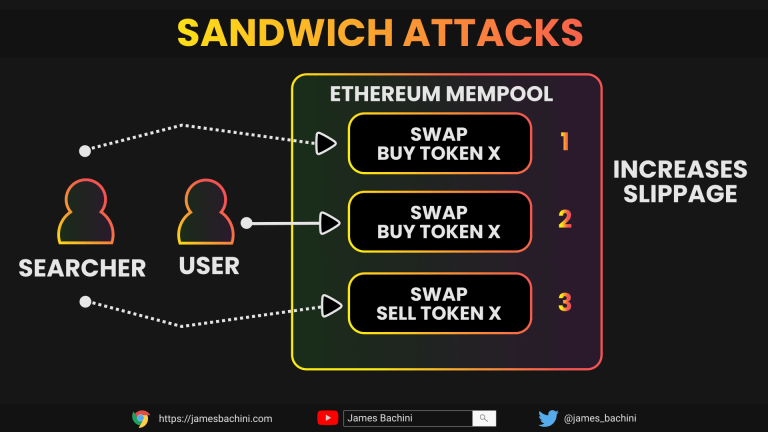

Sandwich Attacks

Front-running combined with back-running forms a sandwich attack. This unethical strategy targets a large trade and tries to encapsulate it.

For example, a sandwich bot spots a large pending buy order for a meme coin on Uniswap. It would buy the token right before the main order (front-running) and would resell it at a higher price (back-running) after causing slippage.

This approach implies three steps:

- The searcher places a buy order right before a pending order, boosting the token price through slippage.

- The victim unknowingly buys the token at a higher price.

- The searcher then sells the token on the DEX, profiting from the price difference.

In this scenario, both the searcher and the victim end up buying the same token, but the MEV bot buys at a lower price while the victim is forced to buy at a higher price due to price manipulation.

In 2023, a searcher made over $1 million in a single day by employing MEV bots executing sandwich attacks. His Ethereum address was responsible for 7% of the gas spent on that day. The searcher remained active in 2024 after improving its tactics.

Not only Ethereum is affected. Last year, a popular MEV bot called “arsc” managed to collect about $30 million in a span of two months by exploiting Solana users through sandwich attacks.

Liquidation Hunting

DeFi lending platforms like Aave or Compound require borrowers to deposit cryptocurrency as collateral, which is liquidated if the use can’t repay the loan or doesn’t cover a certain collateral threshold.

These protocols enable anyone to liquidate the collateral in exchange for a liquidation fee. Searchers use MEV bots to analyze lending protocols and mempools to identify borrowers that can be liquidated. The goal is to use front-running and other techniques to liquidate first and collect the fees.

MEV in Different Blockchain Networks

MEV strategies are lucrative on blockchains with the smart contract feature, which enables them to host multiple decentralized applications (dApps) offering trading and lending opportunities. Therefore, searchers target blockchains that have intense activity, including Ethereum, Solana, and BNB Chain.

Ethereum and MEV

Ethereum is the largest dApp-friendly blockchain. It accounts for over 50% of the total value locked (TVL) in DeFi, which explains why MEV activity is so high on this particular network.

As mentioned earlier, MEV extraction started when Ethereum used the PoW algorithm. Back then, searchers were paying higher gas fees to convince miners to pick their transactions to be added to the next block.

The Future of MEV

MEV, with its advantages and disadvantages, has become an integral part of smart contract chains like Ethereum and will continue to evolve.

As Ethereum is implementing the Pectra upgrade, the third major update following its transition to PoS, the crypto community expects more measures to optimize MEV extraction. Ethereum has been working to implement proposer-builder separation (PBS) directly on the network, similar to what Flashbots has been offering for a while. This is expected to improve the blockchain’s defense mechanism against censorship and bad MEV behavior.

The Pectra upgrade is expected to diversify and streamline validator revenue, as it will enable gas payments using multiple tokens, such as USDC and DAI, and will enable third-party fee sponsorship.

Meanwhile, MEV has been closely monitored by regulators from important jurisdictions, and they may try to restrict it. For example, the European Securities and Markets Authority (ESMA) once labeled MEV as illegal market abuse in its Markets in Crypto-Assets (MiCA) regulation, although the crypto community demands a more nuanced approach, as MEV is not always about unfair exploitation.

In its latest report released in December 2024, ESMA admitted that fourteen respondents to its consultation reacted against assuming that MEV is always market abuse. Therefore, the European Union may take a nuanced approach to MEV, which would be the best-case scenario for the crypto market, as a total ban on MEV can affect validators and other blockchain market participants.

In the UK, the Financial Conduct Authority (FCA) also has a nuanced opinion, stating in a research note:

“The research, both literature review and interviews, indicate there are mixed perspectives over what might be regarded as ‘good’ and ‘bad’ strategies to generate MEV.”

As regulators better understand MEV, they will be able to take targeted actions to address its harmful effect while preserving beneficial aspects. Rather than imposing an outright ban, financial watchdogs may focus solely on MEV strategies like front-running and sandwich attacks.

MEV will remain an unavoidable part of blockchain economics, influencing how transactions are ordered and prioritized on Ethereum. For validators, this can be an extra resource of income, along with newer methods like restaking. However, given MEV’s dual nature, it is imperative to find the right balance between its market optimization potential and unfair exploitation.

In the coming years, the crypto industry must establish the fine line between proliferating MEV’s positive contributions and reducing its harmful effects with surgical precision.